MicroStrategy (now Strategy) made its first Bitcoin purchase on August 11, 2020, when it announced it had purchased 21,454 bitcoins for $250 million. This purchase made it the first publicly-traded company to buy Bitcoin as part of its capital allocation strategy, marking a pivotal moment in corporate adoption of Bitcoin, but it also started something else: the rise of treasury companies.businesswire.com

Analysts and investors are still confused, and for good reason: this type of business endeavor didn't exist before Bitcoin. For some, it disturbingly reminds them of a Ponzi scheme; others see it as a natural consequence of Bitcoin's growth.

While Michael Saylor's giant still holds almost 65% of corporate bitcoins, bitcointreasuries.net lists 168 companies from 29 countries.

There are 23 countries amoung this top 100, but 91.5% of their Bitcoins remain in the US:

In my X article, I briefly describe each company from the top 100:

The Top 100 Bitcoin Treasury Companies: Who Are They?

…but first:

What Is a Treasury Company?

A treasury company is a business whose primary strategy is to accumulate and hold a specific asset rather than generate operational cash flow, often using debt financing to leverage their purchases.

In reality, "the asset" means Bitcoin, which may soon be followed by other cryptocurrencies. That's an important part, because there are two factors that make this model possible for the first time:

- Storing digital assets is very cheap

- Both past and projected annual appreciation is very high

However, if you know anything about business, this may raise your eyebrow: where is the money coming from other than new investors? Why buy a stock instead of buying Bitcoin directly? What is Strategy's "edge"? What is the "end game"?

The Strategy

Michael Saylor's core thesis is that:

- Bitcoin will eventually become the dominant global store of value, similar to how gold functioned historically

- As adoption increases, Bitcoin's price will rise dramatically (he's predicted $1 million+ per Bitcoin)

- The debt interest rates (0-2%) will be far outpaced by Bitcoin's long-term appreciation

In this new world, Strategy becomes a "Bitcoin investment bank"—offering various financial products tied to Bitcoin exposure, transitioning from a software business to essentially a Bitcoin financial services company.

Where Is the Edge?

The question that many Bitcoin lovers have is well represented by macro analyst Andy Constan:

I like Bitcoin. I can understand the bull case. [...] The question is: why should corporations be doing that for their shareholders under what the corporation has? [...] Like where's the edge?

—Andy Constan at What Bitcoin Did

While some buy the stock simply because Bitcoin is not available in their retirement accounts, or for regulatory reasons, for many the edge seems to be the leverage: Strategy's access to cheap debt that is responsible for high mNAV (the multiple of Net Asset Value).

Strategy issues debt in two ways:

Convertible Notes/Bonds

- These were their primary method in earlier years (2020-2022)

- Low or zero coupon rates (0-2% interest)

- Can be converted to equity under certain conditions

Preferred Stock (Multiple Classes)

- STRK, STRC, STRF, STRD - Different classes of preferred shares

- Pay regular dividends (higher obligations than convertibles)

- Some are cumulative (unpaid dividends accumulate), others are not

Preferred stocks are interesting because they're more flexible during a Bitcoin bear market:

- Old model: If convertible bonds matured and couldn't be refinanced, they'd face a liquidity crisis

- New model: They can pause preferred dividends, accumulate the obligations, and resume payments when conditions improve

As Lyn Alden explains:

Preferreds are interesting because it's more of a 'bend and not break' model, which is they have higher quarterly obligations, but those obligations are less immediately catastrophic should they fail to meet those obligations.

Lyn Alden at What Bitcoin Did

Is it completely safe? Not everybody is convinced. Still, the model seems to rely more and more not only on Bitcoin appreciation, but also on new capital inflow. So the question remains:

What is the long-term plan? How does a treasury company plan to make money?

Current Reality: Very Limited Income Sources

Andy Constan asks: "How does a Bitcoin strategy company create income - not capital gains, but income - on their assets?"

One of the ways Bitcoin treasury companies could make money is by running a large Lightning Network node. However, the current scale is still minimal. While LN already processes billions of dollars, fees remain minimal. This will likely not change in the next 5 years.

Bitcoin lending could be another theoretical possibility. While the demand for borrowing Bitcoin remains very limited except for financial arbitrage, it could become viable if Bitcoin becomes more widely used as money.

Will this be enough? If you believe Bitcoin will become global money, you can't rule out this possibility. However, the reality is that this remains the biggest weakness of the investment thesis, and currently mNAV is the only fundamental metric for treasury companies.

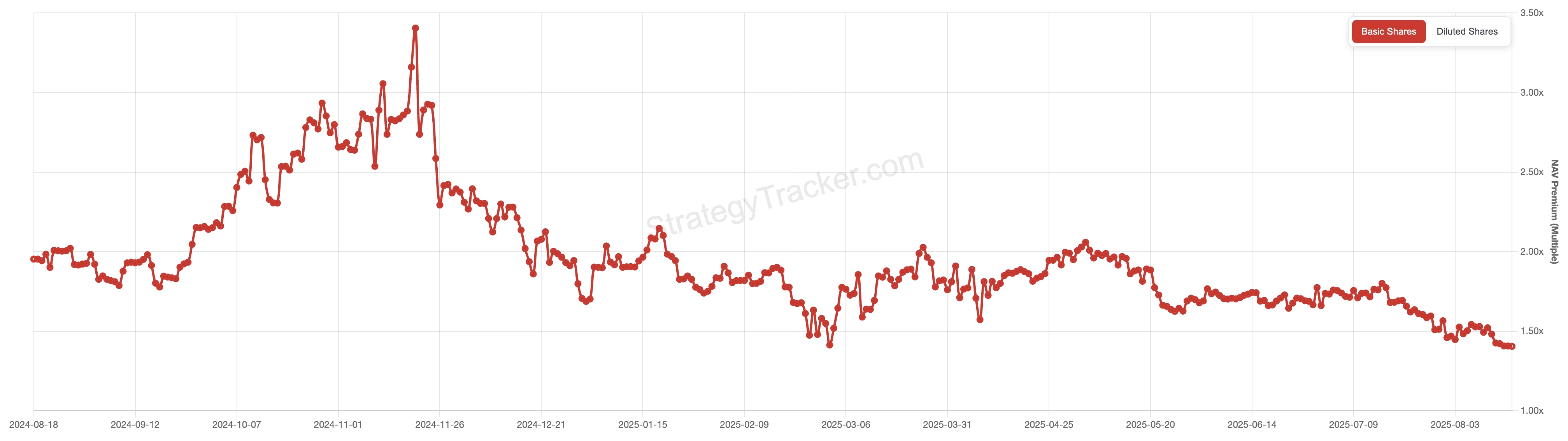

mNAV Premium

The mNAV (multiple of Net Asset Value) is how investors value Strategy relative to its Bitcoin holdings. It's calculated by dividing the company's Enterprise Value by the market value of all Bitcoin it owns. When mNAV is above 1.0, you're paying a premium over the actual Bitcoin value.

The premium exists because investors aren't just buying Bitcoin - they're paying for MicroStrategy's ability to acquire more Bitcoin through debt and equity raises, Michael Saylor's leadership, and access to leveraged Bitcoin exposure they couldn't easily get themselves.

Of course, there's debate about what premium is reasonable.

Lyn Alden thinks 1.2 to 1.8 times NAV makes sense for MicroStrategy, but gets cautious above 2.0x. Andy Constan argues anything much above 1.0x is excessive since you can get leveraged Bitcoin exposure through ETF options without paying extra.

Are Treasury Companies a Speculative Attack on the Dollar?

Saylor openly refers to his Bitcoin thesis as a "speculative attack on fiat."

Bitcoin researcher Pierre Rochard first described the idea of Bitcoin as a speculative attack when it was tiny - that as it grows larger, pools of capital would inevitably find ways to "short fiat currency and be long Bitcoin."

How the "attack" works in theory:

- Cheaply borrow depreciating currency (USD)

- Sell it to buy appreciating currency (BTC)

- Selling USD → increases USD supply

- Buying BTC → decreases BTC supply

- Should push USD/BTC ratio lower (USD weakens vs BTC)

- Your USD-denominated debt shrinks in BTC terms

- Enables more borrowing to continue the cycle

The limitation of this concept is the current scale mismatch: treasury companies hold ~$120B in Bitcoin, which is still not relevant compared to the $27 trillion US bond market. At the moment, despite capturing people's imagination, it remains more of a "meme" than actual mechanics.

Playbook α

Playbook is a premium section with actionable tactics and strategies directly applicable to your portfolio.

In this playbook:

- STRK, STRF, STRD, STRC — Understanding opportunities with new Strategy tickers

Not Only Bitcoin

As treasury companies became a "hot topic," we see more and more companies trying to replicate this model for other assets. For example, Tom Lee's Ethereum Treasury BitMine (BMNR) holds over 1.15 million ETH, while DeFi Development Corp (DFDV) has accumulated over 175,000 SOL. yahoo.com

Proof-of-Stake assets like Ethereum and Solana theoretically offer a significant advantage: staking yield could provide meaningful revenue for the company. However, we can't forget about past currencies like Dash, where despite significant protocol yields, the tokenomics weren't enough to prevent collapse. The model only works if the network continues attracting new capital.

Conclusion

Treasury companies are a completely new market play. The past never fully predicts the future, but in this case we simply lack historical data to model such a future. It's a market bet on hyperbitcoinization, accessible for stock investors and institutions. Remember that even if you strongly believe in the Saylor thesis, the first thing to look at is holding Bitcoin directly. However, treasury companies can be an interesting option to extend your Bitcoin exposure in places where it was previously impossible (retirement accounts), or to benefit from the stability of the fixed income tickers.